The employer may be obliged to pay a transition security contribution if the employer has terminated an employment contract of an employee aged 55 or over on production-related or financial grounds and the employee had been employed by the employer for at least five years. The transition security contributions are used to finance the employee's transition security package. The transition security package consists of two months of transition security training organised by the employment authority for the employee given notice and one month's transition security allowance paid by an unemployment fund to the employee given notice.

The transition security contribution may be payable if the employment contract is terminated on or after 1 January 2023.

The transition security contribution applies to employers whose payroll on which the unemployment insurance contribution is based exceeds the annually specified minimum level. The contribution is based on the Act on the Financing of Unemployment Benefits (in Finnish).

![]()

The employment authority examines the prerequisites for receiving transition security allowance and transition security training and gives a statement on them to the unemployment fund or Kela of the dismissed person. The employment authority provides advice on transition security and transition security training.

Unemployment funds or Kela pay a transition security allowance to a dismissed employee based on the employment authority’s statement. Unemployment funds and Kela provide advice on applying for and paying transition security allowance and on the decision on transition security allowance.

Employment Fund invoices the employer terminating an employment contract for the transition security contribution. The Fund also provides advice on matters related to the transition security contribution.

The employer may be liable to pay a transition security contribution if:

The transition security contribution applies to employers whose payroll on which the unemployment insurance contribution is based exceeds the annually specified minimum level. At the minimum level, the transition security contribution is zero. From the minimum level, the transition security contribution increases linearly to the payroll limit of full transition security contribution.

The transition security contribution is calculated on the basis of the payroll amount for the year preceding the termination.

A State employer’s liability transition security contribution is based on the payroll amount serving as the basis for the employee contributions of an accounting unit or unincorporated state enterprise.

The payroll limits are the same for the employer's liability component and the transition security contribution.

If the company has undergone a merger prior to the day of termination, during the year of termination, or in the year preceding the termination, the transition security contribution is determined on the basis of the merged companies’ total payrolls that served as the criterion for the unemployment insurance contribution of the year preceding the termination.

| Payroll year | Minimum level (EUR) | Maximum limit for full transition security contribution (EUR) |

| 2022 | 2 197 500 | 35 160 000 |

| 2023 | 2 251 500 | 36 024 000 |

| 2024 | 2 337 000 | 37 392 000 |

| 2025 | 2 455 500 | 39 288 000 |

| 2026 | 2 509 500 | 40 152 000 |

The payroll limits are the same for the employer's liability component and the transition security contribution.

The amount of the transition security contribution is determined on the basis of the employer's transition security multiplier. The transition security contribution multiplier, on the other hand, is determined on the basis of the payroll used as the basis for the unemployment insurance contribution. The transition security multiplier increases linearly on the basis of the employer’s payroll.

The transition security multiplier at the limit for full transition security contribution may change annually.

| Year | Multiplier |

| 2023 | 2,90 |

| 2024 | 2,90 |

| 2025 | 2,20 |

| 2026 | 2,20 |

In the formula above, the minimum level of the payroll amount for the year in question is deducted from the employer's payroll amount. The result is divided by the maximum limit for the full transition security contribution from which the minimum level of the payroll amount for the year in question has been deducted. The result is multiplied by the full transition security multiplier.

You can also calculate an estimate of the transition security contribution amount and the transition security multiplier using the transition security contribution calculator.

In addition to the transition security multiplier, the payable amount is affected by the amount of the transition security allowance paid to the employee by Kela or an unemployment fund. .

The transition security contribution is calculated by using the following formula:

The transition security allowance is a benefit calculated and paid by Kela (Social Insurance Institution) or an unemployment fund to the employee given notice. It can be obtained by a person who is:

This is a one-off performance and the amount corresponds to the employee's approx. one (1) month average monthly salary over the past 12 months.

The grounds for the transition security allowance are the salary under insurance paid by the employer terminating an employment contract and other compensation considered as earnings paid on the basis of the terminated employment relationship during the last 12 calendar months preceding the date of termination. The amount of the transition security allowance is calculated by dividing the aforementioned payroll by twelve (12).

As a rule, the transition security allowance is determined on the basis of earnings payment data obtained from the national income information system (incomes register). Earnings under an unemployment insurance contribution will be considered in the payroll. In addition, incomes like holiday bonuses and performance or production bonuses are also included in the payroll. These different bonuses can raise the transition security allowance above the monthly salary. Only wages paid by the employer terminating an employment contract are considered as grounds for the transition security allowance. If a person has salary earnings paid by another employer, they will not be taken into account.

The transition security allowance is determined on the basis of earnings paid in the last 12 calendar months preceding the date of termination, even if this period includes unpaid absences. The average monthly earnings are calculated on the basis of wages paid over full calendar months. For example, if the termination takes place in June, the last paid wages considered will be those paid in May. The calculations are based on contributions. In other words, the time when the wages are earned does not matter. What matters is the time when the wages have been paid to the employee. This 12 months period is not extended in any situation. Unpaid absences or partial paid periods prior to the termination of employment relationship may therefore reduce the amount of transition security allowance. If the employee has not received any salary from the employer that terminates the employment relationship, the transition security allowance cannot be determined, in which case the transition security contribution is not imposed either.

Normally the amount of the transition security allowance is calculated by the employee’s unemployment fund or Kela and they report the amount to the Employment Fund. However, in some rare situations, the liability to pay a transition security contribution may arise even if the person has not been paid a transition security allowance, if their right to transition security training or allowance has been rejected for a reason arising from the person. In this case, the Employment Fund determines the amount of the transition security allowance on the basis of the data on the person’s wages obtained from the incomes register.

The amount of transition security allowance is based on the Unemployment Security Act.

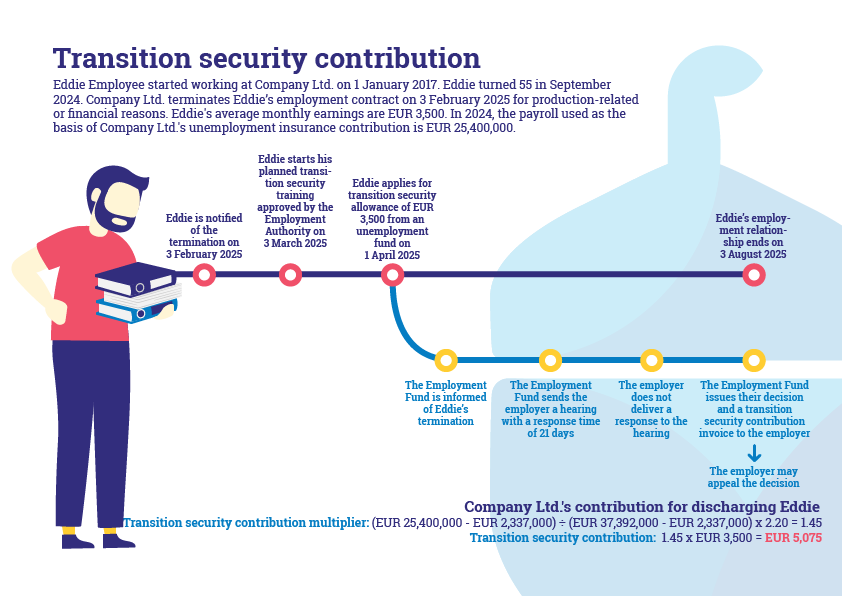

We are notified by Kela or the unemployment fund of a person who has been entitled to transition security or whose right to transition security has been rejected for a reason arising from the person. If we notice that the requirements have been met, we will send a hearing letter to the employer. In the processing stage, we may ask for further clarification from the employment authority, Kela or the unemployment fund, among others.

The employer has 21 days to deliver a response to the hearing letter.

A) The employer does not deliver response or declares that it accepts the contents of the hearing letter:

We issue a written decision on the transition security, obligating the employer to pay the transition security contribution, and we send the employer an invoice for the transition security contribution.

B) The employer delivers a response:

We examine whether there are grounds for exemption from the transition security contribution. To resolve the matter, we may ask for further clarification from the employment authority, Kela or the unemployment fund, among others.

If the employer is not satisfied with the decision, they may appeal to the Social Security Appeal Board. The employer can appeal a decision made by the Social Security Appeal Board at the Insurance Court.

For more detailed instructions see: appeals and refunds of the transition security contribution.

The invoice for the payment of the transition security contribution will be sent to the billing address you have provided for liability component and transition security contribution invoices.

If you have not provided a separate billing address, the invoice for the payment of the transition security contribution will be sent primarily as an e-invoice. The e-invoice will be delivered to the address listed in TIEKE's (Finnish Information Society Development Center) e-invoice directory. If the invoice cannot be delivered electronically, it will be sent to the same address as the decision.

Please note that transition security contribution is directly enforceable. An unpaid transition security contribution can cause an entry in your credit information.

We advise employers on matters concerning the transition security contribution. With regard to matters related to transition security training, advice is provided by the employment authority. With regard to matters related to transition security allowance, advice is provided by Kela and unemployment funds.

See contact information here.

The employer may be obliged to pay the transition security contribution if it has dismissed an employee aged 55 or over on production-related or financial grounds and this employee had been employed by the employer in question for at least five years.

Transition security contributions are collected to finance the extended transition security package, which consists of transition security training corresponding to two months’ pay and organised for the dismissed employee by the employment authority, and transition security allowance corresponding to one month’s pay and paid to the dismissed employee by the Social Insurance Institution of Finland (Kela) or the unemployment fund.

The transition security contribution must be paid by employers whose payroll used as a basis for the unemployment insurance contribution exceeds the annually specified minimum level. The transition security contribution is based on the Act on the Financing of Unemployment Benefits.

The transition security contribution can only be imposed if the employer dismisses the employee on production-related or financial grounds. However, imposition of the transition security contribution does not require that the employment relationship ends on production-related or financial grounds. This means that, as a rule, cancelling the dismissal does not exempt the employer from the obligation to pay the transition security contribution.

However, the employer can submit an application for a refund of the transition security contribution if it has concluded an employment contract valid until further notice with the dismissed employee during the period of notice or the re-employment period referred to in chapter 6, section 6 of the Employment Contracts Act (55/2001) and the employee’s employment relationship continues for at least one year.

Rehiring of the employee by another employer is irrelevant when the transition security contribution is imposed. This is because the employer must pay the contribution if the employee is dismissed on production-related or financial grounds and the other requirements for imposing the contribution are met.

The transition security allowance is paid to the dismissed employee by Kela or the unemployment fund. Payment or recovery of the transition security allowance is not covered by Employment Fund’s advisory services. Contact Kela or the unemployment fund for advice on matters concerning applications for and payment and recovery of the transition security allowance.

The employment authority examines the employee’s eligibility for the transition security allowance and transition security training. The employment authority issues a statement on this matter to Kela or the unemployment fund of the dismissed employee.

The employer may be obliged to pay the transition security contribution even if no transition security allowance is paid to the employee. The employer may be obliged to pay the contribution if, for example, no transition security allowance is paid to the employee because the employee has failed to register as a jobseeker within 60 days of the dismissal.

The employer must pay the transition security contribution if it has given notice to the employee on production-related or financial grounds and the employee then gives notice during the notice period.

The transition security contribution is imposed after Employment Fund has been notified by Kela or the unemployment fund of the employee’s dismissal. Employment Fund usually receives notification of the dismissal within a few months of the termination of the employment relationship. The transition security contribution matter expires when five years have passed from the dismissal of the employee. After that, we can no longer issue decisions on the matter.

You can use the estimation calculator to calculate an estimate of the amount and multiplier of the transition security contribution.

The estimation calculation is only an indication and is not to be regarded as an advance ruling.

If you are dissatisfied with a decision we have made concerning the transition security contribution, you can appeal to the Social Security Appeal Board. You can appeal a decision made by the Social Security Appeal Board at the Insurance Court. Judgments made by the Insurance Court cannot be appealed.

Submit your appeal to us within 30 days of receiving notification of the decision. We will consider the employer to have received the notice on the seventh (7) day after the date when the decision was sent. We will consider State accounting units, municipalities and wellbeing services counties to have received notice on the day when the decision arrives. You will receive more detailed instructions on the appeal process and how to appeal along with the decision.

If we accept the demands set out in the appeal in all regards, we will issue a revised decision. If we are unable to adjust the decision that you are appealing in accordance with your demands, we will submit the appeal to the Social Security Appeal Board.

Note that employers must pay the transition security contribution even if the decision concerning the transition security contribution has been appealed. In such cases, you can petition the Social Security Appeal Board to suspend enforcement, either when you appeal or by submitting a separate application. If your appeal is accepted, we will refund the contribution.

You can file for a refund of the transition security contribution if the employer has concluded an employment contract that is valid until further notice with the employee given notice during the period of notice or the re-employment period referred to in Chapter 6, Section 6 of the Employment Contracts Act (55/2001) and the employee has been in said employment for at least one year.

The employer must apply for a refund of transition security contribution within five years of the earliest date upon which the application could have been submitted.

Apply for a refund on the application form (only in Finnish or Swedish). Attach a clarification to the application indicating the type of employment and when it has started. To receive the refund, please provide the employer's bank account number in our e-services. The account number you provide will be used for all refunds.

Transition security contribution cases expire when five years has elapsed since the termination of the employee. After this, we can no longer issue decisions on transition security contributions.